State Budget 101

By Nick Busse

If you listen to lawmakers from different parties discuss the state budget, it’s easy to be confused. Not only are they debating hugely complex programs in terms that are unfamiliar to most people, but they never seem to agree on the numbers.

If you listen to lawmakers from different parties discuss the state budget, it’s easy to be confused. Not only are they debating hugely complex programs in terms that are unfamiliar to most people, but they never seem to agree on the numbers.

For example, one legislator might say a $34 billion budget would be an increase in state spending; another might argue it’s actually a decrease. Who is right and who is wrong?

To understand the state budget, all you really need to keep in mind are just a few basic concepts. This guide will teach you some of the ins and outs of the budget process and help you understand how to do your own research on taxation and spending.

Budget basics

Every two years, lawmakers and the governor must decide on the state’s biennial budget — how much money the state will spend, and whether any changes are needed to the amount of revenue it collects from taxes and fees.

Under the state constitution, the Legislature is responsible for passing budget bills, sometimes called “appropriations bills” or “omnibus finance bills.” The first year of a legislative biennium (the one right after an election) is devoted to passing a budget.

The budget is enacted when the governor signs all the bills. If changes need to be made later in the biennium, lawmakers can pass what are called “supplemental” appropriations bills to fill in any projected budget gaps.

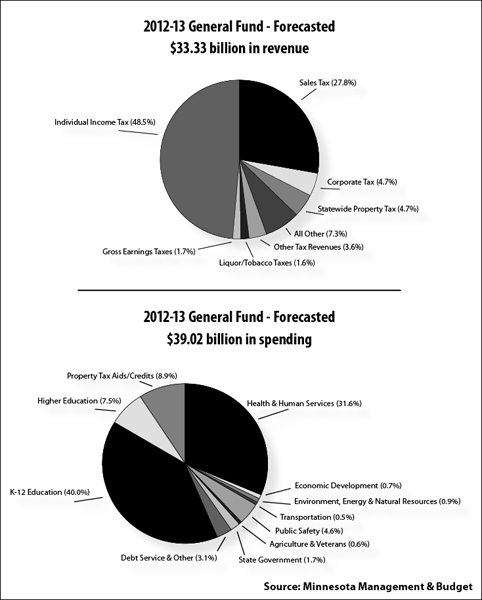

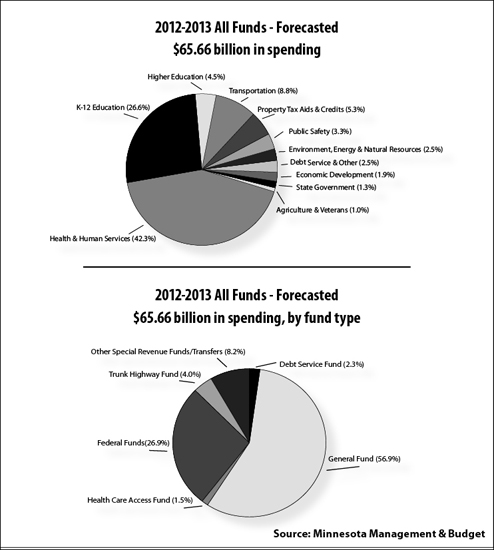

‘General Fund’ vs. ‘All Funds’

One key distinction to understand when talking about the budget is the difference between what’s called the “General Fund” budget and the “All Funds” budget.

The majority of what the state spends comes out of a big pool of money called the General Fund. This is where your state income tax dollars go, as well as revenue from the state sales tax, the corporate tax and several others.

The General Fund gets the most attention when lawmakers are putting together the state budget. This is not only because it’s the largest source of state spending, but also because they have control over what it pays for. The General Fund is used for what’s known as “discretionary spending” — a fancy way of saying legislators can use the money for any purpose they choose.

The General Fund is only one part of the total budget, however. The state also has a number of smaller “dedicated funds” that can only be used for specific things. Often, these are paid for through special taxes and fees. In addition, the state receives money from the federal government that can only be used for specific programs like Medical Assistance or veterans programs.

The combined total of state spending from the General Fund, dedicated funds and federal funds is sometimes called the “All Funds” budget. Because the use of federal and dedicated funds is restricted by state and federal law, lawmakers typically spend less time debating them. But it’s important to remember that they’re a part of total state spending.

Why does the budget grow?

Why does the budget grow?

Not all state spending goes to pay for services provided directly by the state. Most of the money the state spends ends up in the hands of school districts, hospitals, nursing homes, local governments and other programming.

Many things impact the cost of providing public services — the rising cost of health care, for instance. This impacts not only the cost of paying for public employees’ health insurance benefits, but also major state health care programs like MinnesotaCare. Other factors include inflation and growth in state programs due to increased eligibility.

There are different ways to measure growth in the budget. In terms of raw numbers, the state’s all-funds budget has grown from a little less than $37 billion in 2000-2001 to $59.6 billion in 2010-2011 — a 61.1 percent increase. Yet, during that same time, the share of state and local government revenue as a percentage of personal income fell from 16.2 percent in 2000 to 15.3 percent in 2010.

How is this possible? Personal income simply grew at a faster rate than government — not for each and every person, but collectively.

This is not to say that there is a right or wrong way to measure growth in the budget. The point is merely that those who think government should spend less and those who think it should spend more have different ways of making their case.

Forecasted vs. actual spending

Lawmakers often argue over whether a particular budget proposal amounts to a cut or an increase in spending. This is because there are two ways of looking at a budget: one is to weigh a budget proposal against current, or actual, spending; the other is to weigh it against what’s called “forecasted” or “base” spending.

Imagine the state has a health care program that spends $100 million in the current biennium. In the next biennium, budget officials predict that more people will become eligible for the program, raising its forecasted cost to $120 million. If the Legislature funds the program at $105 million in their next budget, is that a reduction or an increase?

The answer depends on your point of view. In terms of real dollars, $105 million is obviously an increase over $100 million. But if the forecasted base funding is $120 million, an appropriation of only $105 million might mean cutting services or tightening eligibility criteria so that fewer people can participate. If you depend on that program for your health care, you might consider it a $15 million cut rather than a $5 million increase.

When listening to legislators debate the budget, it’s important to understand what they’re referring to. Twice a year, Minnesota Management & Budget releases an economic forecast that reflects both current spending levels as well as projected future spending and revenues. You can find the documents on the agency’s website at www.mmb.state.mn.us.

Following the money

Sometimes the best way to figure out what’s really going on in the budget is to see for yourself. Fortunately, there is a wealth of nonpartisan resources available to the public.

Starting with the Legislature, the House and Senate have nonpartisan fiscal analysis staff who provide regularly updated spreadsheets detailing budget bills as they move through the legislative process. These budget tracking spreadsheets can be found on the House and Senate websites. Visit www.house.mn and www.senate.mn and click on the “Publications” tab near the top of the pages.

For even more detailed information on the budget, including economic forecasts and financial reports, MMB’s website provides access to a wide variety of budget related documents. You can find them online at www.mmb.state.mn.us.

Also, if you ever have a question on budget-related activity in the Legislature, don’t hesitate to call House Public Information Services at 651-296-2146 or toll-free at 800-657-3550.

Side note: ‘legislative biennium’ vs. ‘fiscal biennium’

In the Legislature, the word “biennium” often refers to the two-year legislative cycle during which lawmakers serve out their term as elected officials. The term “fiscal biennium,” however, refers to the state’s two year budget cycle. What’s the difference?

The short answer is, about six months. The current legislative biennium began in January of this year, and will end in December 2012. The next fiscal biennium, however, will begin on July 1 of this year and end June 30, 2013. The reason for this distinction is that when lawmakers talk about the state’s biennial budget, they’re referring to the fiscal biennium, not the legislative biennium.

If you’re ever unsure of which is which, just remember that legislative biennia begin with an odd year (i.e. 2011-2012) and fiscal biennia begin with an even year (i.e. 2012-2013).

Side note: borrowing from ourselves

It should be noted that lawmakers sometimes choose to take money out of dedicated funds and use it to shore up the General Fund during a time of deficit. Though legislators from both parties have used the practice, it remains a controversial one. Furthermore, not all special funds can be used in this way, especially those whose purpose is defined in the State Constitution.

Glossary of Budget-Related Terms

Omnibus — refers to bills that contain provisions affecting many different programs, as in “omnibus appropriations bill” or “omnibus finance bill.”

Fiscal Year — the 12-month period beginning July 1 and ending June 30 that serves as the state’s basic accounting cycle.

Fiscal Biennium — two back-to-back fiscal years that together comprise the state’s two-year budget cycle.

Base — Also called “forecasted base.” The amount of money the state is projected to spend, based on current law and economic projections, in a future biennium.

Change Item — refers to changes from forecasted base spending. When the governor or legislative leaders propose a budget, they often include a document with list of change items to make their budget plan more understandable.

Direct Appropriation — spending that lasts for the duration of a fiscal biennium, and no longer.

Statutory Appropriation — spending that remains ongoing from one fiscal biennium to the next unless lawmakers change it.

Open Appropriation — spending that remains ongoing and that is based on a program’s fiscal need rather than a fixed amount.

Standing Appropriation — spends a predetermined annual amount for a specified period of time or indefinitely.

Economic Forecast — a document produced each February and November by Minnesota Management & Budget that estimates expected state revenues and expenditures.

Session Weekly More...

Related Stories

The disappearing budget surplus

Unpaid debts to schools mean the state’s $323 million surplus is fleeting

(view full story)

Published 3/2/2012

Ending the shutdown

Special session ends with compromise that no one really likes

(view full story)

Published 8/11/2011

State Budget 101

A citizen’s guide to understanding the numbers

(view full story)

Published 4/1/2011

Lost in transition

Forecast shows state’s economy is still fragile

(view full story)

Published 3/4/2011

Let the negotiations begin

Dayton budget plan kicks off debate on taxation, spending

(view full story)

Published 2/18/2011

A head start on budget cuts

First bill passed in 2011 would reduce spending by $1 billion

(view full story)

Published 1/28/2011

Two views to ‘unfinished business’

New leaders confront an old foe: the deficit

(view full story)

Published 1/7/2011